Valuation of PKO BP shares based on comparison

of the results of retail banks already quoted at the Warsaw Stock Exchange is an

unfair solution. Obviously, the value of a company depends on estimation of its

future profits. Opinions about PKO BP being expensive compared to other retail

banks as its P/E ratio is x% higher than the average in the banking industry can

indeed tell us something – but about the authors of such an estimate. The most

down-to-earth remark that may be offered here is that an average tells you

nothing, as usually the above average P/E ratio marks companies whose future

results turn higher than average, too. And, by the way, would the estimation

process be interesting at all if it boiled down just to comparing P/E?

Why does PKO BP exist? And other banks as well…

The answer is contained within the bank’s name: the abbreviation stands for

POWSZECHNA Kasa Oszczędności (COMMON Savings Treasury). The company holds a

tremendous advantage of scale compared to its competitors, and the economies of

scale is an effect that cannot be disregarded when talking about a retail bank.

You would find no type of activity in which PKO BP does not take advantage of

its market leadership. The costs of management, computing network development,

promotion, marketing etc are shared by more customers. Each action that PKO BP

undertakes is relatively cheaper than the deeds of its competitors.

The specifics of the retail banking industry provides another kind of advantage

from the economies of scale. For example, the cost of bank transfers for a

customer is usually lower when talking about internal transfers, and often

reduced to zero. Moreover, if money is transferred within one bank, it reaches

the account of destination instantly, without need to wait for the settlement

sessions.

A great number of accounts ran by PKO BP effects in people having their accounts

elsewhere will be forced by their own business surroundings to open one with PKO

BP as well. And the company being a prevailing account provider is true not only

among businesses, but among individual customers as well.

PKO BP needs no special promotion of its accounts, while the best promotional

tool is the fact that such accounts are so widespread, with the majority of

market players having their accounts precisely with this bank. Hence, companies

frequently doing business involving money settlements, even more so if the

settlements involve individual customers, would possess an account with PKO BP

in order to remain competitive. And the higher market share the bank has, the

easier it may increase it further by attracting new customers who respond to the

needs of their environment. Those new customers would create the need of opening

an account in a following group of prospects, and so on. The Polish

anti-monopoly regulations are not a threat here, with a 50% market share being

critical, compared to just twenty-and-some in Germany. Another example of

differing regulations may be British Petroleum forced to sell some of its gas

stations constituting a 4% market share in order for the resultant market share

not to exceed 22%. And, in fact, the like share on the retail banking market

provides more power, due to different product specifics (and lower elasticity)

than in the case of gas stations.

There is no use in trying to reproach the PKO BP clients for choosing this

particular bank. Charging high rates for keeping the account or for transfers is

not in the best interest of the bank, as the first thing that counts is the

scale, where a small unit profit is backed up by high volume of turnover. As a

second thing, extra profits are guaranteed by other products, with an account

being a bait to attract the customer. The anti-monopoly bureau has, as we see,

just a minute chance to contain PKO BP.

The Polish banking system consists of PKO BP and other banks. Those other banks

may not like it; they may not perceive the power of PKO BP as well. But just

like in the case of PZU the strength and value of PKO BP do not stem from the

results recorded so far, but rather from the future profits. The insurance

market and the retail banking market alike are going to grow much faster than

the GDP.

The PKO BP bank has huge room for growth due to expansion of the market and the

economies of scale. Hence its value is many times higher than the one resulting

from estimation based on historical financial record data. The economies of

scale are perceived really well by the anti-monopoly officials in Germany, but

on the domestic market PKO BP will be unstoppable by the anti-monopoly bureau.

It will intercept other banks’ customers with an ease of a running avalanche. Or,

to say it in other words: you can have any bank account you want in Poland,

provided that it is a PKO BP account.

So here we have one issue of the market share that PKO BP has and the resulting

economies of scale, with another issue being the size of the market. The value

of banking services is still many times lower in Poland than it is in the

countries of the EU-15, and so are the personal debt levels, both face value and

compared to annual income. The retail banks will feel the results of an economic

warm-up later than the ones servicing large and medium businesses, but then

those are precisely the retail banks whose profit out of the warm-up will be the

greatest. The industrial market is much more competitive, whereas the retail

banks, especially the largest ones, just take advantage of their sales networks.

For private customers and small businesses the basic criterion for choosing the

bank is the access to it through an account, and not the differences in interest

rates or commission values. PKO BP has a broad depository base, which means

access to cheap money. In the future the other side of the equation – increase

in credit base – will be provided as well, and this will be the less demanding (and

more common) part of credits for small businesses and private customers.

PKO BP includes an offer for the up-market customers as well. Internet banking

accounts are offered to all the account holders, with PKO BP suddenly having

become the largest internet bank in the country. Still few of the PKO BP

customers are using this option, but those who want it, do have such an option.

This is a profitable combination indeed!

CA IB report on PKO BP – a ‘miscarriage of valuation’?

A few days ago, CA

IB issued a report determining the value of a PKO BP share to be 21.7 PLN. It is

a common knowledge that CA IB is a strange bank in a sense, having become famous

by means of HOOP S.A. and IMPEL S.A. offerings and valuations. In both the cases

mentioned, the bank, being at the same time the offerer, has grossly

overestimated share values. Taking into account the upturn in index values, the

overestimation was as high as 200%, which means that for the CA IB valuations to

be true the HOOP and IMPEL shares would have to be three times as expensive as

in reality! There is more to read about CA IB in an editorial from

Rzeczpospolita: http://polandsecurities.com/ca-ib.html

Now it seems that CA IB in turn grossly underestimated the value of PKO BP,

which is being indicated by the market. A ‘miscarriage of valuation’? Ones

adverse to the company claim something different.

The Ministry of Treasury is being criticized for how the privatization of PKO BP

was conducted. The charges of having sold PKO BP at a price much lower from the

one that could have been obtained start to be justifiable. Moreover, the

Minister of Treasury admitted that “social causes” did influence the price. More

about the PKO BP privatization:

http://polandsecurities.com/pko.htm

The Ministry let a multitude of petty investors profit. In fact, the ones that

both had some ready cash and queued to get the scarce good – with the queues

taking after ‘social list’ and rationed sale – did profit. The ones that

possessed PKO BP – that is the whole society – lost. The ones that earned at the

cost of all others were the people queuing in front of the bank branches (which

is not a derogatory remark – they have acted in a really rational way, on a ‘if

they give – take it’ basis), stockbrokers and banks charging commission on loans

provided to make up for predicted reductions. Good entertainment for public

money… The way PKO BP was privatized is depicted best with a single question: a

sabotage or mere foolishness?

And then the CA IB report appears, evaluating the PKO BP shares to be worth 21.7

PLN in line with the Minister’s opinions. At the same time, the CA IB Financial

Advisors Sp. z o.o. and CA IB Securities S.A. are invited to place bids for a

limited tender designed to choose an Advisor to the Ministry of Treasury for PZU

S.A. privatization. The CA IB CEO, Ms Alina Kornasiewicz, has already privatized

PZU once… Apparently together with Minister Socha she wants to move forward this

“successful” privat(e)-ization.

CA IB concluded a deal with PZU recently, resulting in at least a 100m PLN loss

on the side of PZU according to opinions of analysts and investment advisors.

The market was shocked by the underrated total for a purchase of shares of three

NFI (National Investment Funds). You can read more about the transaction in and

editorial from Parkiet:

http://www.polandsecurities.com/raport/pzu

As a reward, CA IB was invited to place a bid in a tender to appoint an advisor

to deal with the PZU privatization. The Ministry’s actions could be called

grotesque if it was not for the fact that, that the whole society has to pay for

such “entertainment”, including people much less opulent than Ms. Kornasiewicz

or Mr. Socha. An invitation to CA IB regarding the deal with PZU should indeed

have been issued – but and invitation to the prosecutor’s office.

The stock market environment sometimes witnesses deals that are widely named

‘white collar crimes’. Yet sometimes such crimes happen, that could be nicknamed

‘snatch-and-run deals’ as well.

And an accusation of such a crime is more than relevant in the case of PZU and

CA IB deal.

Apparently, Ms Alicja Kornasiewicz will not disclose any more information on the

details of deal with Eureko and the attempt to sell control of PZU for a

fraction of its value and against the tender procedures until the Judgment Day.

The environment should, nevertheless, eliminate people suspected of deals

resulting in damage to the Treasury, even more so when credibility of such a

person and the organization that he or she leads slumps and public

recommendations issued by it indicate at the very least lack of knowledge in the

area of company valuation.

Jacek Socha is apparently trying to continue the Eureko mega-deal, and as he

invites Ms. Kornasiewicz to cooperate, he fails to see anything suspicious in

the CA IB and PZU deal (or, if he saw something, he chose not to boast about

communication with the prosecutor’s office).

PKO BP value

Taking into account the law restrictions on compiling recommendations here I

will quote the opinions of some investors I know. The think that, considering

prices of other banks quoted on the stock exchange, the value of PKO BP shares

is about 40 PLN. Such price rate represents the fair value of the bank. I share

their opinion fully.

The estimate regards current bank share prices. If those prices of retail banks’

shares increases, the estimate should be elevated as well. Approximately, a fair

value of PKO BP would be 40 PLN + or – the change in the WIG Banki index.

The regulations regarding compilation of free reports came into being right

after the HOOP SA IPO, when the Commission for Securities and Stock Exchange

reproached a practice of issuing reports critical towards the company about to

go public. The issuers’ reports provided estimates of HOOP SA value much above

the IPO price (provided by CA IB, DI BRE Bank and JPMorgan). The only

independent report, written by me, having resulted in rescheduling the IPO,

valued the shares according to the company book value. It considered the other

estimates, a few times higher than the book value, to be irrelevant. Currently,

the value of HOOP SA is indeed oscillating around the book value per share.

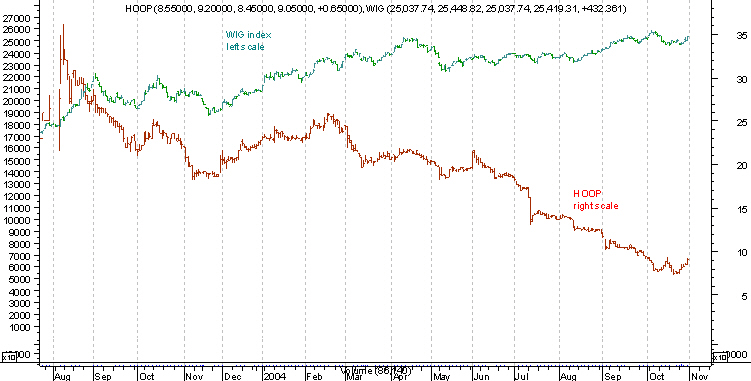

The people who believed the CA IB and DI BRE Bank reports and paid 4 time the

book value per share have apparently lost. Here is a chart presenting HOOP SA

quotations:

http://polandsecurities.com/hoop-vs-wig.jpeg

A side story on TVN

Currently, such companies as CA IB, BRE Bank and JPMorgan are linked to the TVN

SA share issue. The ITI Holdings owners, including BRE Bank, will record income

from the shares sold.

At the same time, the ITI founders and financial shareholders support an

elevated valuation of TVN, being the main asset of ITI. Not only do they hold

TVN and ITI shares, but also… TVN and ITI debts.

A bankruptcy of TVN would affect the portfolios of a few friendly entities by an

amount of several billion PLN, standing for the paper valuation of TVN and ITI

shares as well as debts of both companies. That is why one should say that the

TVN shares sold in the IPO or simply moved ‘from one portfolio to another one’.

Most probably, adverse conditions meaning lack of demand on the side of private

investors would result in purchase of shares by friendly entities. Swapping the

shares like this costs nothing and provides an opportunity to create any kind of

a ‘market’ price the participants want. Due to higher necessity (the need of an

‘appropriate’ valuation of TVN) small investors, being the ones who responded

best to the IPO, still have a chance to quit their commitment. Here you will

find more about TVN

http://www.ipo.polandsecurities.com/tvn-ipo.pdf [in English]

One should remember that bubbles grow really nice, but then they burst in an

even more fashionable manner, and it is the public, not financial institutions,

that are lured by small amounts of air-filled soap, very often broadly

advertised ahead of an IPO.

We might recollect, to be precise, that Hoop, sold for 21 PLN during the IPO,

reached the price 35 PLN during the first few sessions at the Warsaw Stock

Exchange, and as much as 100 PLN much earlier when quoted at the Central Table

of Offers, while the current quotations are just about 9 PLN.

Another interesting detail of the last days linked to the BRE Bank portfolio, is

the forecast of bleak results of Q4 2004 by the BRE Bank. One would rather

expect a huge improvement of a credit portfolio and capital investments

resulting from the general warm-up of the economy, with such a forecast

indicating best the kinds of treasures that BRE Bank possesses.

Sidewise, the way of realizing the asset value is a plainly strange thing here.

One would expect the assets to be monitored on a current basis, as required by

the banking law, but also by basic principles of bookkeeping. If those assets

lost their fair value in another quarter, the results of it had to be, at least

to say, not too true. Do the assets of BRE Bank really lose their value during

economy warm-up, then?

Jaroslaw Suplacz

29.12.2004

Adres Redakcji i Wydawcy:

ul. Szarych Szeregów 18/20, 09-409 Płock

Redaktor naczelny i Wydawca:

Jarosław Supłacz

Miejsce i data wydania:

Płock, 29.12.2004

{kind=link}